Building significant wealth is an achievement. Preserving it across generations requires a different level of planning.

For ultra-high-net-worth families, estate taxes are rarely a theoretical concern. They are a known liability—often substantial, often due quickly, and often payable at the worst possible time. Without intentional planning, taxes and liquidity constraints can quietly erode decades of value creation.

Life insurance, when structured correctly, remains one of the most effective tools available for protecting family wealth, maintaining control, and ensuring assets transfer as intended.

This article explores how sophisticated families integrate life insurance into estate planning to address estate taxes, liquidity challenges, and long-term legacy objectives

How Estate Taxes Can Create Risk for Even the Most Successful Families

At death, federal and state estate taxes may be assessed on the total value of an estate. These taxes are generally due within nine months, regardless of whether the estate holds sufficient cash to pay them.

For many families, this creates a liquidity problem, not a wealth problem.

Assets are often concentrated in:

- Closely held businesses

- Commercial or residential real estate

- Long-term investment holdings

- Private equity or alternative investments

When taxes come due, families may be forced to:

- Sell operating businesses

- Liquidate investments at unfavorable market conditions

- Dispose of real estate quickly

- Take on high-cost debt

The result is often permanent value destruction, family conflict, and loss of control. Estate taxes do not need to be avoided entirely to be damaging—poor timing alone can change outcomes for generations.

Life Insurance as a Liquidity Strategy, Not a Product

Life insurance is uniquely positioned to solve estate tax liquidity issues because it delivers capital exactly when needed.

However, the benefit is not the policy itself—it is how ownership and control are structured.

When properly designed, life insurance can:

- Create immediate liquidity at death

- Preserve operating businesses and long-term assets

- Prevent forced sales

- Provide predictability in an otherwise uncertain tax environment

When structured incorrectly, life insurance can increase estate taxes rather than reduce them.

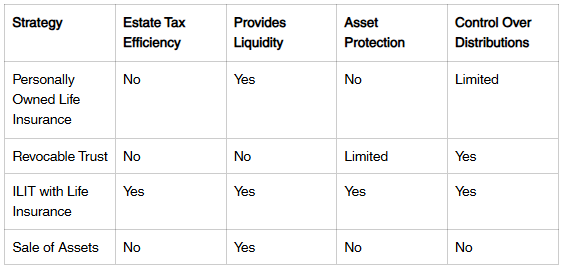

Ownership Is the First Critical Decision

If an individual owns their life insurance policy personally, the death benefit is generally:

- Income-tax free

- Included in the taxable estate

For large policies, this inclusion can materially increase estate tax exposure.

The solution is not the policy itself—it is removing ownership from the insured’s estate.

The Irrevocable Life Insurance Trust (ILIT)

An Irrevocable Life Insurance Trust (ILIT) is the primary vehicle used to exclude life insurance from the taxable estate.

When established and administered correctly:

- The trust owns the policy

- The insured does not retain incidents of ownership

- The death benefit is excluded from the taxable estate

- Proceeds pass to beneficiaries free of estate tax

How an ILIT Works

- An ILIT is drafted and executed by estate planning counsel

- The trust applies for and owns the life insurance policy

- Premiums are funded through properly structured gifts

- At death, the trust receives the death benefit

- Liquidity is deployed according to trust terms

The trust may be designed to:

- Pay estate taxes

- Purchase assets from the estate

- Equalize inheritances

- Provide long-term asset protection

- Govern multigenerational distributions

Why ILITs Are a Cornerstone of Advanced Estate Planning

For ultra-high-net-worth families, ILITs offer several structural advantages:

- Estate tax exclusion: Insurance proceeds remain outside the taxable estate

- Liquidity at the right time: Capital is available when taxes are due

- Asset protection: Trust-owned assets are shielded from creditors and divorce

- Control: Distribution terms reflect family values and long-term intent

- Privacy:Trusts avoid public probate processes

The result is not just tax efficiency—it is continuity.

Funding an ILIT Without Creating Gift Tax Issues

Proper funding is essential. Premiums paid incorrectly can undermine the entire structure.

Common funding techniques include:

- Annual gift tax exclusions

- Crummey withdrawal provisions

- Strategic use of lifetime exemption when appropriate

These mechanisms allow policies to be funded efficiently while minimizing or eliminating gift tax exposure. And administrative discipline matters—missed notices or improper payments can compromise the trust.

Advanced Uses of Life Insurance in Estate Planning

Equalizing Inheritances

When one heir receives an operating business and another does not, life insurance can create economic balance without disrupting control of the enterprise.

Business Succession and Continuity

Life insurance can:

- Fund buy–sell agreements

- Provide working capital at death

- Prevent forced liquidation

- Stabilize ownership transitions

Multigenerational Legacy

Trust-owned life insurance may benefit children, grandchildren and future descendants. When structured properly, this capital can avoid future estate taxation and support long-term family objectives.

Common Mistakes That Undermine Life Insurance Planning

Even well-intentioned plans fail due to execution errors:

- Personal ownership of policies

- Transferring existing policies and dying within three years

- Poor trust drafting

- Inconsistent beneficiary designations

- Failure to coordinate insurance with broader estate plans

These mistakes can reintroduce estate taxes and invite unnecessary scrutiny.

Who Benefits Most from Life Insurance Estate Planning

This planning is particularly relevant for families who:

- Have substantial net worth

- Own closely held businesses or real estate

- Prefer privacy and control

For these families, planning early provides flexibility that is unavailable later.

Final Thoughts: Plan Before It Is Required

Life insurance is not merely a benefit, it is a strategic planning tool.

When ownership is structured correctly, trusts are properly administered, and planning is done well before a triggering event, life insurance can preserve wealth, protect heirs, and maintain control across generations.

The most significant estate planning risk is not complexity—it is delay. Start planning now to protect your wealth and secure your family’s legacy.

Studemont Group, LP is not a law firm and does not provide legal advice. Estate planning strategies should be implemented in coordination with qualified legal and tax counsel. We work alongside your advisors to help design and implement appropriate life insurance structures.

John McDonough is the founder and President & CEO of Studemont Group, the Houston-based wealth preservation advisory firm he founded in 2010. With more than 25 years in the industry and Texas General Lines licensure held since 2001, he focuses on the advanced planning that complex estates demand — premium financing, irrevocable life insurance trusts (ILITs), estate tax liquidity, and business succession — coordinated into a single strategy rather than sold as separate products. A dedicated educator through the JMac Wealth channel, he works alongside clients’ attorneys and CPAs to help families and business owners protect, preserve, and transfer wealth across generations.

Related Posts